Monthly Interest For 1 Lakh Fixed Deposit: Calculation With Latest Rates

Debt There are quite a few investment options: conventional and alternative, but for millions of Indian investors, fixed deposits remain the most preferred choice. They are considered a dependable avenue for individuals who prioritise capital safety and predictable returns. Whether you are a salaried professional, a retiree, or a conservative investor, fixed deposits provide stability and assurance without exposing your savings to stock market volatility.

One of the most common questions investors ask is: “How much interest can I earn monthly on an INR 1,00,000 fixed deposit?” Understanding the potential monthly income from a fixed deposit can help investors better plan their finances and create a reliable source of supplementary cash flow.

Here you will learn how the monthly interest for a 1 lakh fixed deposit is calculated, compare different return rates based on the interest earned on fixed deposits, provide general information on the taxation of fixed deposits, and explore alternative ways to generate a higher monthly return. For ease of comprehension, you will get fixed deposit payout options throughout.

How FD Monthly Interest Is Calculated

The interest earned on a fixed deposit depends on three key factors: the deposit amount, the applicable interest rate, and whether the interest is paid on a cumulative or non-cumulative basis. Each of these variables plays an important role in determining total returns and payout frequency for the investor.

You can select either a cumulative FD (interest is compounded and paid when the FD matures) or a non-cumulative FD (interest is paid monthly, quarterly, etc.).

Monthly income from FDs is generally calculated using the simple interest formula:

Interest annually = Principal x Rate of Interest

Interest paid monthly = (Principal x Interest rate) / 12

If you invest INR 1,000,000 at an interest rate of 7% for 12 months:

- Interest in the first year = INR 7,000

- Monthly Income = Interest / 12 = INR 583

Therefore, the monthly income from a fixed deposit of 1,000,000 at 7% would be (INR 7,000) or approximately INR 583.

If you invest INR 1,000,000 at an interest rate of 8% for 12 months:

- Interest in years = INR 8,000

- Month Payout = INR 8,000 / 12 = INR 667

You can use this method to manually determine your monthly income from a fixed deposit in India.

Calculation Using Online FD Calculators

Online fixed deposit calculators offer a simpler and more efficient alternative for personal financial planning. These tools automatically factor in variables such as interest rates, compounding frequency, tenure, and payout structure, helping investors quickly and more accurately estimate their expected returns.

You can use the 1 lakh FD monthly interest calculator available here:

You can determine your expected returns by entering your principal investment, interest rate, and the time your deposit will remain open. This will allow you to compare cumulative and regular monthly payments.

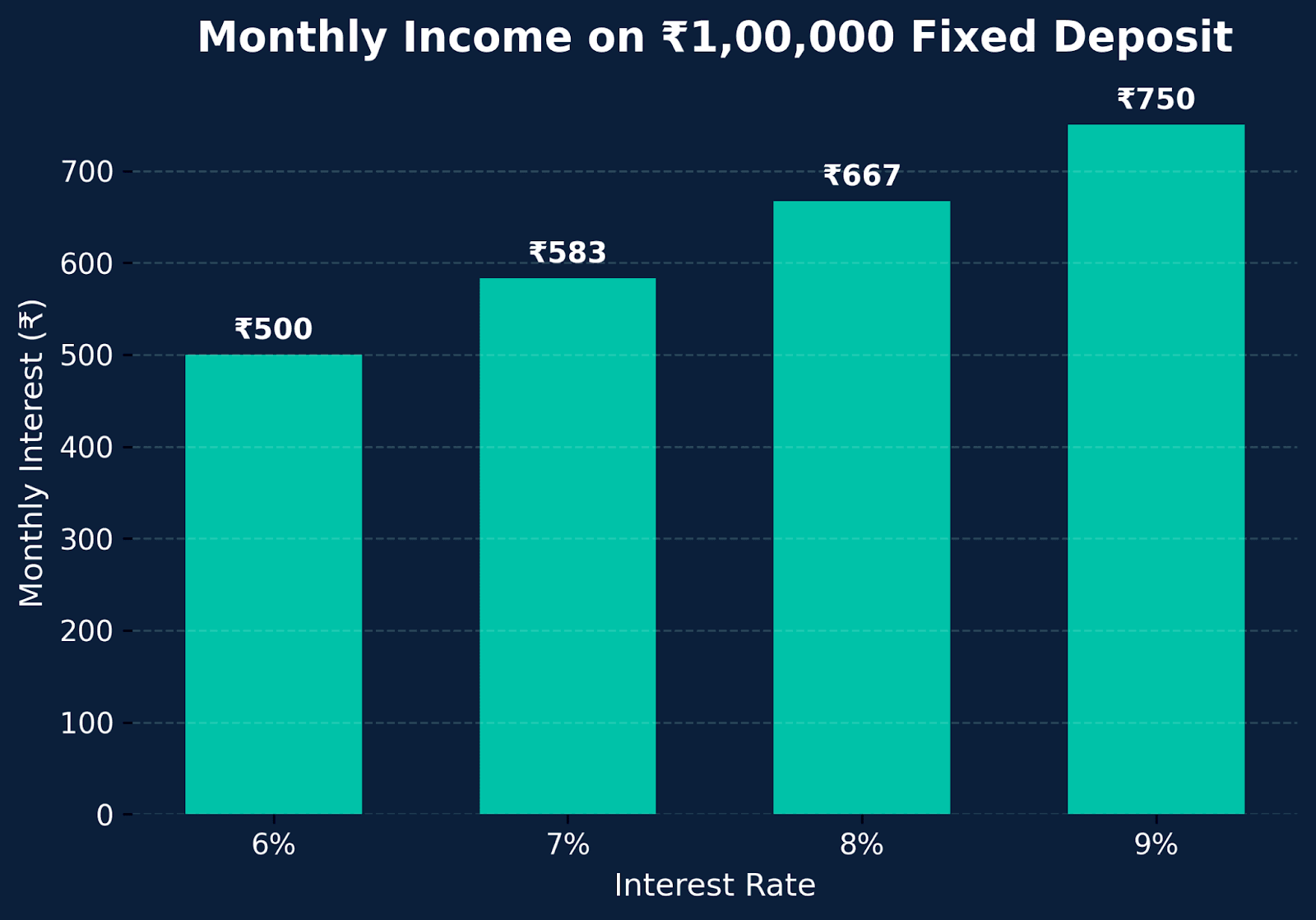

Monthly Interest For 1 Lakh At Different Interest Rates

Interest rates vary based on tenure and investor category. Below is a comparison table:

| Interest Rate | Annual Interest | Monthly Payout |

| 6% | INR 6,000 | INR 500 |

| 7% | INR 7,000 | INR 583 |

| 8% | INR 8,000 | INR 667 |

| 9% | INR 9,000 | INR 750 |

As seen above, a 1% increase in interest rate can significantly increase your FD monthly income in India over time:

Senior Citizen Variation

Seniors typically qualify for an increase of 0.25% to 0.50% over standard rates on their deposit accounts. In this example, 8.5% vs. 8%, you would receive the corresponding FD monthly income India.

- Annual interest: INR 8,500

- Monthly payment: INR 8,500 ÷ 12 = INR 708

The extra interest could make a significant difference in your overall monthly financial picture during retirement.

Tax Deduction On FD Interest

Interest earned on fixed deposits is taxed under the head “Income from Other Sources.” It is added to your total income and taxed according to your applicable income tax slab.

If the interest earned exceeds the prescribed threshold in a financial year, the bank automatically deducts Tax Deducted at Source (TDS). Please consult your tax advisor for the exact details on TDS and the impact of FD interest on your tax return.

Here is an example of how tax affects your FD interest.

Let us say your annual interest from your fixed deposit (FD) is INR 8,000 and that you are in the 20% tax bracket.

Your taxes owed will be 20% of your total annual FD interest, or:

- The tax owed = 20% of INR 8,000 = INR 1,600

- Your net annual interest = INR 8,000 - INR 1,600 = INR 6,400

So your net monthly income from this FD is INR 6,400 divided by 12 months, which is INR 533.

Alternatives For Higher Monthly Income

While fixed deposits are widely regarded as a safe and reliable investment option, their returns may not always keep pace with inflation, particularly if your goal is to generate a higher monthly income. In such cases, it may be worthwhile to diversify a portion of your savings into other income-generating investments.

For instance, corporate bonds and secured non-convertible debentures (NCDs) offered by platforms like Grip Invest often yield more than traditional fixed deposits, while debt mutual funds can provide relatively better, tax-efficient returns over time. Additionally, for investors with a moderate risk appetite, dividend-paying stocks and hybrid funds can serve as effective options for generating regular income while also offering the possibility of capital appreciation.

By maintaining a balanced approach and allocating funds across different asset classes, investors can enhance their income potential while still preserving overall portfolio stability. You can also check some more alternatives to fixed deposits on this blog.

FAQs

1. How much interest for a 1 lakh FD per month?

A one lakh fixed deposit will earn around INR 583 in monthly interest if the rate is 7% per annum and about INR 667 if the rate is 8% per annum. This will vary depending on the interest rate and the frequency you want to receive payments.

2. Is a monthly payout better than a cumulative FD?

If you need a monthly income, the fixed deposit with a monthly payout is better for you. However, if you want to accumulate a large sum of money by saving and allowing it to compound until the end of your Fixed Deposits, the cumulative Fixed Deposit is preferable.

3. How is FD interest taxed?

Based on your income tax bracket, fixed deposit interest income is taxable, and TDS may be deducted on interest payments exceeding a certain threshold. As a taxpayer, it is your responsibility to report the interest income even if TDS is not deducted.

Want to stay at the top of your finances?

Join the community of 4 lakh+ investors and learn more about Grip Invest, the latest financial knick-knacks, and shenanigans in the world of investing.

Happy Investing!

Disclaimer - Investments in debt securities/municipal debt securities/securitised debt instruments are subject to risks including delay and/ or default in payment. Read all the offer related documents carefully. The investor is requested to take into consideration all the risk factors before the commencement of trading.

This communication is prepared by Grip Broking Private Limited (bearing SEBI Registration No. INZ000312836 and NSE ID 90319) and/or its affiliate/ group company(ies) (together referred to as “Grip”) and the contents of this disclaimer are applicable to this document and any and all written or oral communication(s) made by Grip or its directors, employees, associates, representatives and agents. This communication does not constitute advice relating to investing or otherwise dealing in securities and is not an offer or solicitation for the purchase or sale of any securities. Grip does not guarantee or assure any return on investments and accepts no liability for consequences of any actions taken based on the information provided. For more details, please visit www.gripinvest.in

Registered Address - 106, II F, New Asiatic Building, H Block, Connaught Place, New Delhi 110001